Top 7 Questions About Debt Settlement and Credit Score

- UpdatedDec 9, 2024

- How does debt settlement affect your credit score?

- Normally, entering debt settlement drops your score -- at first.

- As debt settlement progresses, client credit scores rise -- and keep rising after graduation.

Table of Contents

- 1. What is debt settlement?

- 2. What happens to my credit score when I begin a debt settlement program?

- 3.What is “debt burden” and why does it matter?

- 4. Does the Freedom Debt Relief program permanently harm my credit score?

- 5. How can my credit score go up if I settle for less than I owe?

- 6. What happens to my score after I graduate from Freedom Debt Relief?

- 7. What are the other financial benefits of completing a debt settlement program?

- Is debt settlement right for you?

If you’re looking for a way to deal with your debt, you may be considering a debt settlement program. And, during your research, you may find information saying that it can harm your credit score. While this is true in the short-term, in the long-term your creditworthiness is more than just your credit score. For example, decreasing your heavy debt burden is a key factor in establishing a not just a better credit score, but also a better financial future.

So what is the real impact of debt settlement on credit score? To answer this question, we conducted a four-year study with help from one of the three leading credit bureaus to find out what really happens to the credit scores of Freedom Debt Relief (FDR) clients during and after their program.

The results might surprise you.

The study found that once a client completes the Freedom Debt Relief program, they have:

A reduced debt burden

After an initial drop in the first six months, clients’ credit scores begin to recover

A credit score that has recovered to nearly the same level as it was at the start of the program

Improved financial habits

Read on to get more answers to the seven top questions people ask about the relationship between debt settlement and credit scores.

1. What is debt settlement?

Debt settlement is the process of working with creditors to get them to accept less than the amount owed on a debt to consider it resolved. When you work with a debt settlement company (like Freedom Debt Relief), they negotiate with your creditors on your behalf to reduce your debt. Debt settlement companies do charge a fee for providing this negotiation service, but it cannot be charged up front, only after you have reached a settlement with your creditor.

In a debt settlement program, you:

Voluntarily stop making payments on all the accounts you enroll which signals to your creditors that you are in financial distress and opens up the opportunity to negotiate a settlement

Make monthly deposits into a special FDIC-insured savings account, which are used to fund settlement payments to your creditors

Review the terms of each negotiated settlement and provide authorization

As the debt settlement program progresses, accounts will get settled one by one, until all of the enrolled accounts have been paid off and resolved.

2. What happens to my credit score when I begin a debt settlement program?

Making on-time payments to creditors is one of the most important factors that affect credit score. When you enroll in a debt settlement program, in order to be able to negotiate with your creditors, you will stop paying on the accounts you enroll. As a result, your credit score can drop during the early months of a program. If you’re used to thinking of your credit score as a measure of your financial health, this can seem a little daunting.

However, after about six months, your credit score can begin to improve. This is typically the time you start authorizing settlements and when debts begin to get resolved. In addition, our study showed that the majority of the credit scores of Freedom Debt Relief graduates recovered to where they were at the time of enrollment by the end of their program. Remember, your credit score assesses your credit worthiness at a given point in time. As the debt settlement process improves your financial situation, your credit score can begin to recover.

3.What is “debt burden” and why does it matter?

Debt burden is a more general way of referring to the amount of debt you have. One of the most influential variables for credit scores like the FICO® Score is credit card utilization. Credit card utilization is calculated by taking the total outstanding balances on your credit cards and dividing them by your total credit card limits. You can then multiply by 100 to get a percentage. The greater your credit card utilization, the higher your minimum payments become. In turn, this can make it even harder to keep up with payments for all of your bills.

As a consumer, a high debt burden means that too much of your income is going to pay off debt. That’s money that can’t be used for things like saving up for a home, a college fund, retirement, or emergency expenses. Even if you can keep up with your debt payments, having too much debt keeps you from being able to save.

One of the advantages of a debt settlement program is that, over the course of the program, debt burden goes down while credit score recovers. This graph illustrates how this works for Freedom Debt Relief graduates:

FDR Graduates Reduced Debt Burden*

The numbers at the bottom of the graph are months, from the start of the program to the end of a 4-year program. In this example, the median Freedom Debt Relief client starts with around $28,000 in debt at the time of enrollment, and that goes down to $3,800, 45 months after enrollment. Meanwhile, the credit score starts at 650, drops to around 500, then gradually rebounds to around 650.

4. Does the Freedom Debt Relief program permanently harm my credit score?

No. The negative impact to Freedom Debt Relief clients (who complete the program) is usually temporary. As stated above, scores drop in the first months, then start a steady recovery as settlements are authorized and accounts are resolved through the course of the program. Around the time of graduation from the program, their credit score is close to the same as it was when they began.

As you can see in the graph below, Freedom Debt Relief graduates enter with a median credit score of 650, experience a drop in credit score in the first six months of their program, and then see a rebound in credit score to 648 near the end of their program, which is typically around 48 months.

FICO® Score Recovery

Additionally, it is important to understand that negative information will not remain on your credit report indefinitely. Most negative information is removed from your credit report 7 years after the incident, while some events like bankruptcy, can remain on your report for 10 years.

5. How can my credit score go up if I settle for less than I owe?

Two important factors that affect credit score are credit card utilization and payment history, which together account for 65% of your score. Debt settlement can help improve both of these factors in the longer term. Here’s how:

Credit card utilization

Credit card utilization refers to how much of your available credit you’re currently using. For example, if you have one credit card with a $20,000 credit limit and your balance is $10,000, your credit card utilization for that account is 50%. Higher credit card utilization tends to be associated with greater credit risk and therefore, lower credit scores. Many credit scores take into account credit card utilization across all your accounts.

Payment history (delinquency rate)

On-time payments help your credit score, and late or missing payments (called delinquencies) hurt your score. Creditors view late payments as a sign of financial distress, so when you first start a debt settlement program and stop paying your creditors, your payment history can take a hit, potentially affecting your score. But as you progress through the debt settlement program, and accounts are resolved. those late payments “age” and can have less of an impact on your score.

Many people considering a debt relief program have a high credit card utilization ratio; this is one reason why many Freedom Debt Relief clients have a credit score below 700 when they start the program. Over the course of the program, your credit card utilization should begin to decrease, helping your score recover.

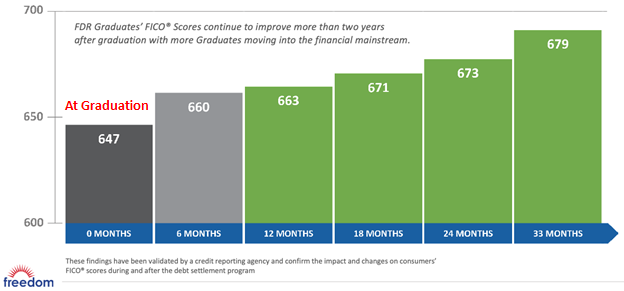

6. What happens to my score after I graduate from Freedom Debt Relief?

The study shows that many of the Freedom Debt Relief graduates continued to experience improving credit scores after their time in the program. Here is one more chart illustrating how Freedom Debt Relief graduates’ FICO® scores can continue to go up more than two years after graduation.

FICO® Score Recovery Post Program

7. What are the other financial benefits of completing a debt settlement program?

Your credit score changes as your financial situation changes, so the biggest impact on your score in the future will be driven by how you handle your finances and your debt.

To keep your score as strong as your circumstances allow, make sure you understand the top 5 credit score factors, and implement healthy financial habits. Being a client in the Freedom Debt Relief program can help you develop these better skills, as it requires you to:

Make a consistent monthly program deposit building a savings discipline

Delay non-essential purchases until you have the money to pay cash

Reduce or eliminate reliance on credit cards

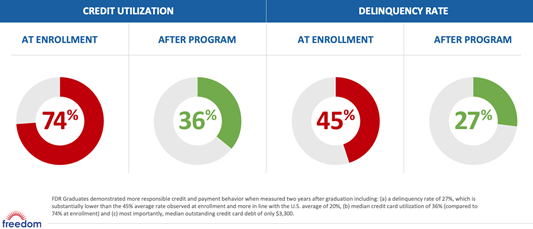

This responsible behavior is often reflected in graduates’ FICO® scores. For example, when the study looked at credit utilization and payment history for clients two years after graduation, the median credit utilization dropped from 74% to 36%, and payment delinquency rate dropped from 45% to 27%. This is a great example of the smart debt management habits graduates learn and continue — even years after completing the program. Here is what that looks like:

FDR Graduates’ Responsible Credit Behavior

Debt is a huge financial burden for many Americans, and eliminating it is the first step to helping build a stronger financial foundation that can serve them for years to come.

Is debt settlement right for you?

The study results we’ve featured here are based on the median outcomes — results that are in the middle of what was experienced by clients included in our four-year study. Individual results vary depending on specific financial circumstances, creditors, and type of debt.

So if you are considering debt relief, we recommend you speak to one of our Certified Debt Consultants. They’ll go over your financial situation with you and help you determine if the Freedom Debt Relief program makes sense in your situation. The consultation is free — and you can get started right here.

Learn More

Credit Report vs. Credit Score – What’s the Difference? (Freedom Debt Relief)

5 Steps to Build Your Credit from Scratch (Freedom Debt Relief)

Does Unemployment Affect Your Credit Score? (Freedom Debt Relief)

How to Protect Your Credit Score During the COVID-19 Recession (Freedom Debt Relief)

A look into the world of debt relief seekers

We looked at a sample of data from Freedom Debt Relief of people seeking debt relief during October 2024. This data highlights the wide range of individuals turning to debt relief.

Age distribution of debt relief seekers

Debt affects people of all ages, but some age groups are more likely to seek help than others. In October 2024, the average age of people seeking debt relief was 49. The data showed that 15% were over 65, and 17% were between 26-35. Financial hardships can affect anyone, no matter their age, and you can never be too young or too old to seek help.

Collection accounts balances – average debt by selected states.

Collection debt is one example of consumers struggling to pay their bills. According to 2023, data from the Urban Institute, 26% of people had a debt in collection.

In October 2024, 30% of debt relief seekers had a collection balance. The average amount of open collection account debt was $3,203.

Here is a quick look at the top five states by average collection debt balance.

| State | % with collection balance | Avg. collection balance |

|---|---|---|

| District of Columbia | 23 | $4,899 |

| Montana | 24 | $4,481 |

| Kansas | 32 | $4,468 |

| Nevada | 32 | $4,328 |

| Idaho | 27 | $4,305 |

The statistics are based on all debt relief seekers with a collection account balance over $0.

If you’re facing similar challenges, remember you’re not alone. Seeking help is a good first step to managing your debt.

Manage Your Finances Better

Understanding your debt situation is crucial. It could be high credit use, many tradelines, or a low FICO score. The right debt relief can help you manage your money. Begin your journey to financial stability by taking the first step.

Show source