Do You Need to Change Your Spending Habits?

UpdatedApr 16, 2025

- Mindless overspending can derail your budget and get you into trouble with debt.

- Review your spending and look for bad habits to change.

- If your debts are too high, find out if you qualify for a debt relief program.

Overspending is incredibly common. In fact, a 2023 NerdWallet survey found that even among Americans with a budget, 84% ended up spending more than the limits they had set for themselves.

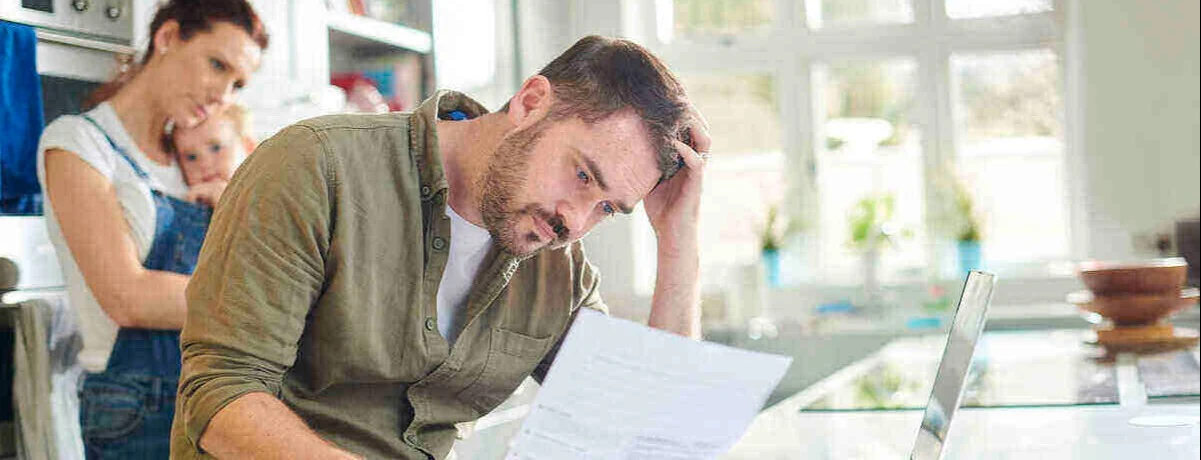

Overspending can interfere with your ability to accomplish your financial goals. It can also cause you to go deeply into debt. Learn how to watch for signs that you need to change your spending habits.

Here are a few things to be on the lookout for, along with some tips on how to change your spending habits for good.

Signs you need to change your spending habits

You're spending too much on small stuff

One easy way to know if you need to change your spending habits is to ask yourself, “Where does my money go each month?” If you don't know the answer, you may be spending too much on small stuff.

The reality is that you probably don't notice all the small purchases you make over time. However, these purchases can add up quickly and leave you with less money for important financial goals. If you cut spending on these little purchases, that could have a major positive impact on your finances.

Auditing your spending is a great way to reduce the little expenses and change your spending habits for good. To do that:

Take a look at your bank account or credit card debt statements

Create a spreadsheet, or grab a notebook and start writing down your expenses, organizing them into categories, such as groceries, dining out, or online orders.

Identify the things you're spending the most money on. This might be frequent shopping trips, food in restaurants, or particular kinds of purchases.

Set spending limits on each category, especially those where you regularly spend too much.

Once you've done this, if you really want to change your spending habits, you need to regularly track your spending. Weekly spending check-ins could help you become more mindful of overspending and focus your money on more essential expenses.

You don't have a financial routine

If you don't have systems for managing money, chances are much higher that you'll overspend.

A budget routine is a great way to change your spending habits. At the end of each month, look back at the income you brought in and how much you spent. This allows you to forecast your spending for the upcoming month. You could also do this weekly or every other week if you need more help limiting spending.

In addition to a budgeting routine, start regular financial conversations with your significant other, if you have one and they’re part of your financial landscape. Talking about money more often could reduce the likelihood you'll fight about the topic. It also gives you an accountability buddy to help you stick to spending limits.

Your credit card debt is creeping up

If your credit card debt doesn’t come down over time, or worse, if it rises, that’s a sign that you’re living above your means. It’s unsustainable. At some point, you’re likely to lose the ability to charge more. It’s also a very expensive way to fund a lifestyle.

Reducing spending can be hard for anyone. We all like to be able to buy what we want. Even so, imagine how much extra money you could have in your budget if you weren’t paying interest on credit card debt—possibly even enough to afford to pay cash for the things you’re charging.

If you’re relying on your credit cards because of a financial hardship, such as a job loss, that’s understandable. Credit is a great way to bridge a short-term financial gap. But if your credit card debt is lingering because of your spending habits, that’s something to look at. You’re hurting yourself by not letting yourself get ahead financially.

How can you change your spending habits?

Now you know how to determine if you need to change your spending habits. But how can you put changes in place and stick with them? Taking these steps can make it easier to break bad habits and spend less.

Create small wins

Starting with big goals can feel overwhelming, and a simple setback could cause you to give up. You're much more likely to succeed if you break big goals down into small ones that are manageable and measurable, and that you can achieve quickly.

For example, you might be tempted to do a spending freeze in which you completely stop spending money on non-essential things—but this isn't a lifestyle most people want to stick with. Instead, try starting small, and celebrating the progress you make.

For example, if you love making a daily coffee shop run, switch to making your own coffee just once per week to start changing the habit. Replacing even one day of buying coffee with making your own brew adds up over time, and as you see how much you save, you may be inspired to make coffee at home even more often.

Coffee might not be your thing. Look at your own spending and try to spot little luxuries that you would be willing to live without. Your sacrifices don’t have to be permanent.

Visualize progress

Visualizing your progress is another great way to change your spending habits.

For example, if you want to spend less at the grocery store, track your spending there. Your tracker can be as simple as a sheet of paper that you keep on your refrigerator door. Record the date, grocery store, and the amount spent each time you get back from buying groceries.

With the tracker showing you exactly how much you have spent, you can spot improvements in real time and might be inspired to look for more ways to save. You may even decide to get creative with the food you already have on hand to come up with quick meals that stretch your budget further.

You can implement this strategy with any spending cuts you want. Suppose you're prone to picking up takeout dinners. Record on a sheet of paper every time you go, where you went, and how much you spent. Keep the sheet of paper where you can see it, like in your car console. The visual reminder could be just the thing you need to skip the drive-thru once or twice this week.

Focus your energy on one thing, not many things

There are many moving parts to your financial life, and you may want to tackle multiple goals. However, when you try to address too many things at the same time, it’s harder to make progress.

If you want to change your spending habits, focus your energy on accomplishing that goal before shifting to a different one, like exploring your debt consolidation options or learning more about investment opportunities. Once you've changed your spending habits, it should be easier to tackle the next goal.

Start changing your spending habits today

Deciding to change your spending habits is a worthy goal. It can help set you on the path to many other financial successes. So get started today.

Take a close look at your budget, look for spending cuts you can make, and track your progress. Once you're spending less, you can use money you've freed up to begin working on other goals that matter to you.

Debt relief stats and trends

We looked at a sample of data from Freedom Debt Relief of people seeking debt relief during November 2024. The data uncovers various trends and statistics about people seeking debt help.

Credit card tradelines and debt relief

Ever wondered how many credit card accounts people have before seeking debt relief?

In November 2024, people seeking debt relief had some interesting trends in their credit card tradelines:

The average number of open tradelines was 14.

The average number of total tradelines was 24.

The average number of credit card tradelines was 7.

The average balance of credit card tradelines was $15,142.

Having many credit card accounts can complicate financial management. Especially when balances are high. If you’re feeling overwhelmed by the number of credit cards and the debt on them, know that you’re not alone. Seeking help can simplify your finances and put you on the path to recovery.

Collection accounts balances – average debt by selected states.

Collection debt is one example of consumers struggling to pay their bills. According to 2023, data from the Urban Institute, 26% of people had a debt in collection.

In November 2024, 30% of debt relief seekers had a collection balance. The average amount of open collection account debt was $3,203.

Here is a quick look at the top five states by average collection debt balance.

| State | % with collection balance | Avg. collection balance |

|---|---|---|

| District of Columbia | 23 | $4,899 |

| Montana | 24 | $4,481 |

| Kansas | 32 | $4,468 |

| Nevada | 32 | $4,328 |

| Idaho | 27 | $4,305 |

The statistics are based on all debt relief seekers with a collection account balance over $0.

If you’re facing similar challenges, remember you’re not alone. Seeking help is a good first step to managing your debt.

Support for a Brighter Future

No matter your age, FICO score, or debt level, seeking debt relief can provide the support you need. Take control of your financial future by taking the first step today.

Show source

How can you control the habit of spending too much?

There are many ways to take control if you overspend. You could live on a budget. You could establish a 24-hour rule and commit to thinking about something you want to buy for at least 24 hours before making the purchase. You could enlist an accountability buddy, or get professional help from a financial advisor or debt relief expert. The key is to find an approach that works for you.

How do I change my spending habits?

For many people, the first step in changing their spending habits is tracking spending and creating a budget. If you monitor your spending, know where your money is going, and set limits to rein in overspending, you can make positive changes.

Why do I have bad spending habits?

You may have bad spending habits for many reasons. You may not have received much financial education, or you may have learned bad habits from your parents. It's also sometimes just really hard to live within your means, and it's tempting to spend too much because so many things are expensive.

You should identify your own reasons for overspending, and work to take control of them and make a positive change.