Ohio Debt Relief by the Numbers: 5-Year Debt Trends

Although the average cost of living in Ohio is 17.3% lower than the national average, many Ohioans are struggling with debt.

In 2024, the median income in Ohio was about $72,200. And the average person in Ohio owed about $45,800 in debt as of 2024, according to the Center for Macroeconomic Data. In comparison, the average debt on a national level in 2024 was $62,000.

If you're overwhelmed by debt in Ohio, know you aren’t alone. Data shows that many people in Ohio are having a hard time managing their debt—but help is available.

We’ll review recent debt trends in Ohio among people who’ve sought debt relief with Freedom Debt Relief. We’ll look at how their credit card, auto loan, and installment loan balances have changed, and what you can do if you’re struggling to manage debt.

Ohioans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

5-Year Debt Trends in Ohio

Thanks to inflation, many Americans are living paycheck to paycheck these days, and that’s led a lot of people to fall behind on their debt. Debt relief seekers in Ohio saw their debt increase from $23,197 in 2020 to $30,750 in June 2025—a nearly one-third increase.

The average minimum monthly debt payment among Ohio debt relief seekers rose from $1,280 in 2020 to $1,692 in June 2025—a 32% increase.

The good news is that FICO Scores increased among Ohio debt relief seekers. In 2020, their average score was 554, and as of mid-2025, it was 592. That’s well below the average 715 credit score among Americans overall, according to Experian. However, it’s in line with the average 592 credit score among debt relief seekers across the U.S.

Meanwhile, debt relief seekers in Ohio had an average debt-to-income (DTI) ratio of 30.4% in 2021. As of June 2025, that number had risen to 38.5%. On a national level, debt relief seekers had a DTI of 42.3%, so Ohio debt relief seekers may not be spending quite as much of their income on debt payments as their peers across the U.S.

However, total debt is on the rise in Ohio. Between 2021 and mid-2025, total unsecured debt among Ohio debt relief seekers (including credit card balances, installment loans, and student loans) rose from $69,186 to $77,213.

Secured debt (including mortgages and auto loan balances) among relief seekers increased from $182,996 in 2020 to $183,637 in June 2025. And their average total debt (secured plus unsecured) rose from $245,166 to $260,850 in the same time period. On a national scale, total debt among debt relief seekers in mid-2025 was $345,211.

Interestingly, among low-income Ohio debt relief seekers, debt levels actually fell slightly—from $20,674 in 2020 to $20,483 in 2025. But among moderate-income Ohio debt relief seekers, debt levels rose from $24,742 in 2020 to $26,745 in June 2025, an 8% increase.

Among debt relief seekers with poor credit in Ohio, average debt fell from $37,837 in 2020 to $28,056 in June 2025. Many people found themselves out of work in 2020 when the pandemic drove unemployment levels up to an extreme degree, so that could explain the decrease in overall debt among poor-credit debt relief seekers.

Finally, in mid-2025, debt relief seekers in Ohio ages 65 and over had the highest average credit score at 606. Those ages 51 to 65 had the next highest score at 593, and borrowers 18 to 25 had the lowest score at 563. However, older borrowers tend to have the benefit of a longer credit history to raise their scores.

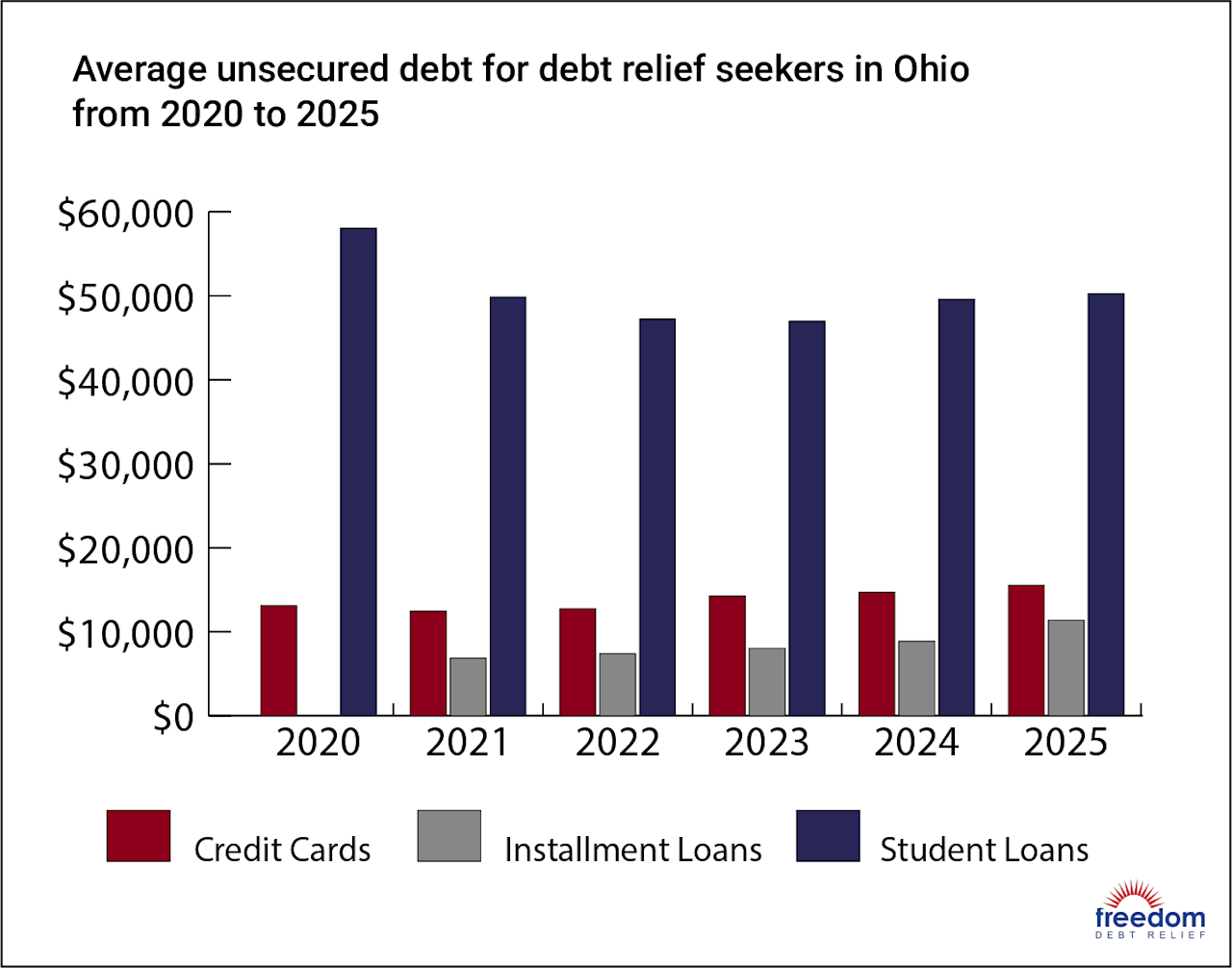

Ohio credit card debt

Among debt relief seekers, average credit card balances rose from $13,094 in 2020 to $15,541 in June 2025. That's lower than the average credit card balance of $16,244 among debt relief seekers nationwide as of the same date.

The average monthly credit card payment increased substantially for Ohioans seeking debt relief. In 2020, it was $392, and it rose to $494 in mid-2025. That's a bit below the average monthly $489 credit card payment among debt relief seekers nationally as of June 2025.

Credit utilization, meanwhile, dropped among Ohio debt seekers, going from 88.8% in 2020 to 75.4% in June 2025. That's a bit above the national average of 73.50% for U.S. debt relief seekers. High credit utilization could lead to a lower credit score, and make it hard to keep up with credit card payments.

The average number of open credit card accounts held by debt relief seekers in Ohio rose from 7.5 to 7.8 during that same five-year period. That's a bit above the national average of 7.4 among debt relief seekers throughout the country.

Credit card debt can be difficult to pay off because credit cards typically come with very high interest rates. Credit card interest can also compound frequently, making it easy for that interest to rack up against you. If you’re struggling to keep up with credit card debt, it could pay to seek credit card debt relief.

Ohio auto loan debt

Among debt relief seekers, the average auto loan balance in Ohio rose from $21,301 in 2021 to $24,630 in June 2025. That's not far from the average auto loan balance among debt relief seekers nationally, which was $26,997 in June 2025.

Meanwhile, the average monthly auto loan payment among debt relief seekers in Ohio rose from $563 to $696 during that same time period, marking a change of 23.6%. Despite that increase, that $696 average monthly payment is lower than the average monthly auto loan payment of $749 among debt relief seekers nationally.

Ohio mortgage debt

Among debt relief seekers, the average mortgage balance in Ohio went from $182,996 in 2020 to $159,007 in mid-2025. That’s well below the average mortgage balance of $239,406 for debt relief seekers nationally.

The average monthly mortgage payment among debt relief seekers in Ohio decreased from $1,717 in 2020 to $1,457 in June 2025. On a national scale, debt relief seekers had an average mortgage payment of $1,989 in June 2025.

Ohio installment loan debt

Among debt relief seekers in Ohio, the average installment loan balance rose from $6,863 in 2021 to $11,384 in mid-2025, marking an almost 66% increase. However, that average loan balance for June 2025 was lower than the average installment loan balance among all U.S. debt relief seekers of $12,632.

The average monthly installment loan payment for Ohio debt relief seekers, meanwhile, rose from $333 in 2021 to $430 in June 2025. That's lower than the average monthly installment loan payment among national debt relief seekers, which is $485 as of that date.

Ohio student loan debt

Among debt relief seekers, the average student loan balance in Ohio fell from $58,076 in 2020 to $50,289 in June 2025. That's a bit higher than the average student loan balance among debt relief seekers across the U.S., which was $49,932 in June 2025.

Ohio debt relief seekers had an average monthly student loan payment of $226 in 2021. The monthly average payment rose to $316 in mid-2025, while on a national scale among debt relief seekers, the average monthly student loan payment for the same time is $313.

If you’re struggling to repay your federal student loans, you may be eligible for relief in the form of forbearance, deferment, or an income-driven repayment plan.

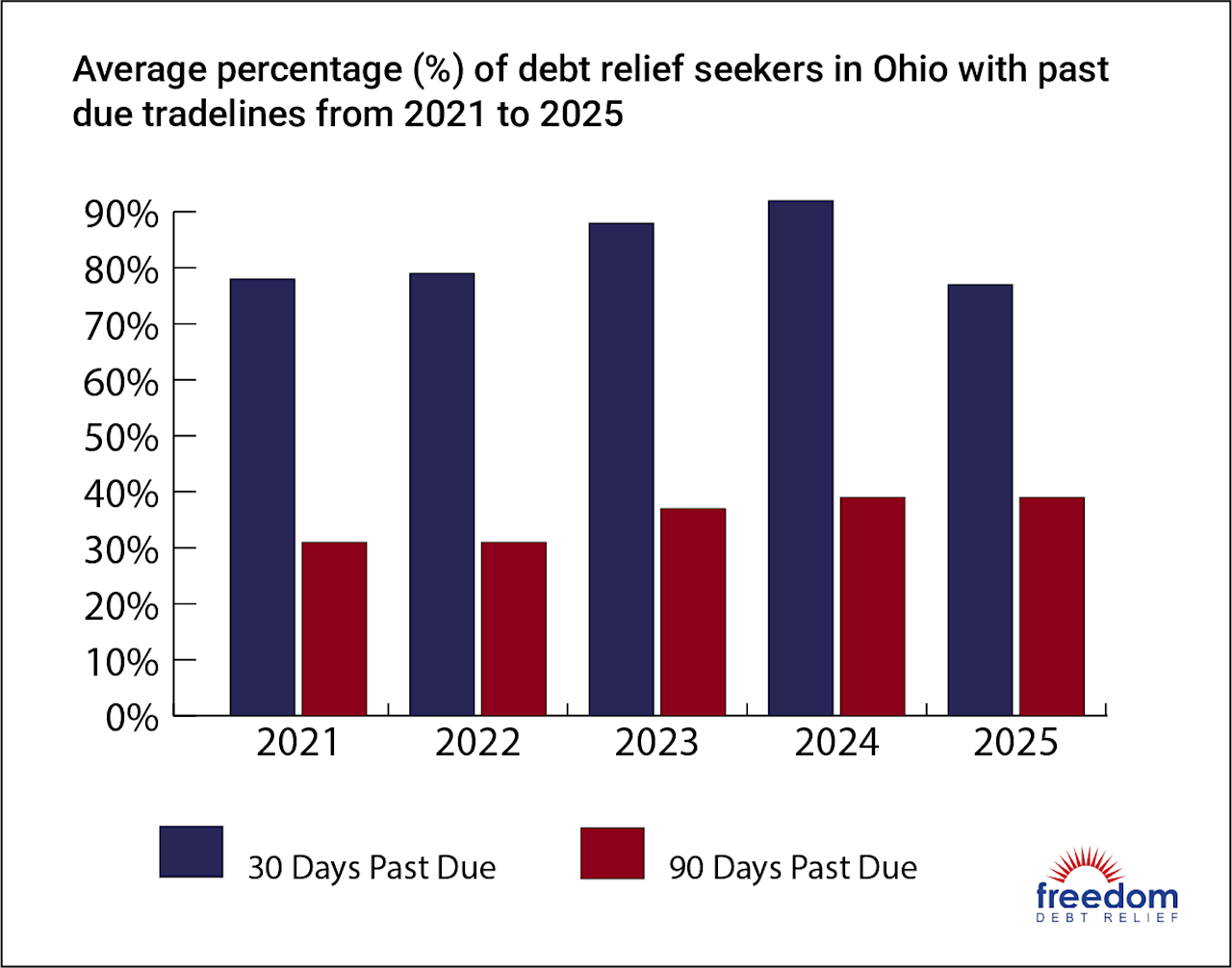

Ohio Debt Delinquencies and Collections

Among debt relief seekers in Ohio, there were 3.6 accounts in collections on average in 2021, compared to 2.0 in June 2025. The average balance in collections also fell from $3,171 in 2021 to $2,577 in June 2025. Among debt seekers nationally, the average collections balance was $3,040 as of that date.

It’s not just debt relief seekers who are falling behind on their debt. Here’s how all Ohio residents are faring in terms of delinquencies, according to data from TransUnion.

| Type of debt | 30-plus days past due | 60-plus days past due | 90-plus days past due |

|---|---|---|---|

| Auto loan | 4.22% of consumers | 1.64% of consumers | Data not available |

| Credit card | 4.60% of consumers | 3.25% of consumers | 2.36% of consumers |

| Mortgage | 2.95% of consumers | 1.41% of consumers | 0.90% of consumers |

The longer a debt is past due, the bigger the impact it can have on a credit score. Also, with secured debts like auto loans and mortgages, borrowers who are past due run the risk of repossession or foreclosure.

Ohio Statute of Limitations

A statute of limitations is the window of time in which a creditor can successfully sue you to collect an unpaid debt (they might try even after the statute runs out, but the debt would be considered “time-barred,” which should mean the suit is dismissed). Here’s an overview of Ohio statutes:

| Type of debt | Ohio statute of limitations |

|---|---|

| Credit cards | 6 years |

| Medical debt | 6 years |

| Personal loans | 6 years |

| Auto loans | 6 years |

Generally, the statute of limitations clock starts on the date of your last payment. For installment loans like personal or auto loans, the clock starts on the date your payment is due.

What are the Ohio debt collection laws?

The Fair Debt Collection Practices Act and the Ohio Consumer Sales Practices Act work together to protect consumers from abusive and unfair debt collection practices.

In Ohio, a debt collector must send you a letter within five days of reaching out by phone. The letter has to state the amount you owe, who you owe it to, and the amount of time you have to dispute the debt.

You generally have 30 days from when a debt collector contacts you to dispute a debt or request that they go through the debt verification process. You can instruct debt collectors not to contact you again.

Debt collectors may not call you at an unreasonable hour, harass you, or use threatening language. They also cannot tell others about your debt.

Reviews and Testimonials from Ohio

My experience was great because of Rafael M who was my debt consultantant and Terri who was my customer welcome specialist. Beyond the great services that you offer, these two specialists made my experience very comfortable and easy. Please give them my sincere thanks and give them props!

Jason Jerome, US

Everyone from customer Svc to the loan department explained the settlement process and the communication with e- mail really kept me informed

Gerald Lovejoy, US

Everyone was nice and thoughtful. They answered all my questions

Joseph Pavel, US

Ohio Debt Relief

If you have overwhelming debt, a debt relief program could be a good way to manage it. With a debt relief program, a debt settlement company negotiates with creditors on your behalf. You typically make a monthly deposit into a dedicated account, and that money is used to negotiate settlements.

A debt relief program is typically suitable for people who are behind on their debts and don't have a path toward paying off those debts in full. It can take two to four years to complete.

If you want to learn more about your debt relief options in Ohio, contact Freedom Debt Relief to request a consultation. A Debt Consultant can speak to you about your financial situation, and possibly refer you to a program that’s appropriate for your situation.

Is Debt Consolidation the Best Debt Solution?

If you’re struggling with debt but aren’t missing payments, debt consolidation may be a good fit for you. Debt consolidation is when you take a new loan and use it to pay off more than one smaller debt. It could make your debts easier to manage by lowering the number of monthly payments.

Better yet, if you can lower the interest rate on your debt, it might be more affordable. If you have a lot of high-interest credit card debt, you may be able to lower your interest rate by paying it off with:

A personal loan

A 0% balance-transfer credit card

A home equity loan or line of credit

Debt consolidation could make the most sense if you:

Have a strong enough credit score to qualify for a debt consolidation loan or balance transfer credit card

Know you’ll be able to pay off the new debt

Other Debt Relief Alternatives in Ohio

Here are some other debt relief options that may be all or part of the solution for your situation:

Debt settlement. Negotiate with your creditor to accept less than the full amount you owe, but consider it payment in full. Debt settlement is for someone who has a financial hardship and can’t afford to fully repay their debt.

Hardship programs. These are arrangements some creditors offer to make it easier to pay what you owe. They may include delaying or reducing monthly payments, suspending late fees, or lowering your interest rate.

Income-driven student loan repayment plans. You might have the option to enroll your federal student loans in a payment plan that’s based on your income. This can help you afford student loan payments even on a low income.

Credit counseling. A nonprofit credit counseling agency can help you enroll in a debt management plan. Creditors typically agree to lower your interest rate, but you can’t use credit cards while you’re in the program. You make one payment to the agency and they distribute the money to your creditors. There is no debt forgiveness.

DIY debt payoff. You can pay off your own debts at your own pace by setting a budget and allocating money to your debt every month. Common strategies for this include the avalanche method, in which you pay off your debts from highest interest rate to lowest, or the snowball method, in which you pay off your debts from smallest balance to largest.

Bankruptcy. A court decides how to use your income or assets to settle your debts to the extent possible. If it’s a fit for your circumstances, bankruptcy gives legal protection from creditors.

Ohioans can free up cash each month with Freedom Debt Relief

Ozzy S., Freedom client²

“Right away, I had more money each month because of program costs so much less than what I was paying on my minimums.”

Excellent •

What are the different types of debt consolidation options available in Ohio?

You’ve got several different options for debt consolidation in Ohio. The right choice for you will depend on your specific financial situation.

You could consolidate your debt into an unsecured personal loan, which comes with fixed monthly payments. Or, if you own a home, you could look at consolidating your debt into a home equity loan or cash-out refinance mortgage.

A balance transfer credit card may also be an option for debt consolidation, and these offers typically come with a 0% introductory interest rate. But be careful, because if you don't repay your entire balance by the end of your introductory period, your interest rate will skyrocket.

You may also be able to work with a credit counseling agency and get a debt management plan (DMP), where you make a single monthly payment. Agencies that offer these plans typically charge a fee for their services.

A debt settlement program is not debt consolidation, but it’s similar in that you could make a single monthly deposit into an account where you build up funds for offering your creditors.

What are the typical interest rates for debt consolidation loans in Ohio as of October 2025?

The interest rate you pay on a debt consolidation loan will depend on a number of factors, including the type of loan you take out, the amount of your loan, and your credit score.

If you're taking out an unsecured personal loan, the stronger your credit score is, the lower an interest rate you may be able to qualify for. Working to boost your credit score before you take out a debt consolidation loan could result in lower payments each month while you're paying your loan off.

Personal loans are a popular choice for debt consolidation. Depending on your credit score, you might pay anywhere from about 7% to 36%.

That's a very wide range, so if you're looking to consolidate your debt, you'll need to shop around with different lenders and find out what rate they offer you on a loan. From there, you can calculate what your monthly payments would be to determine if the loan would be affordable.

What credit score is generally required for a debt consolidation loan in Ohio?

The credit score you need to qualify for a debt consolidation loan in Ohio will depend on your lender and the specific type of loan you're taking out. Personal loans are a popular type of debt consolidation loan, but they're also unsecured. This means they’re not tied to a specific asset that a lender can sell or repossess, like a home or car, to get its money back.

If you're taking out a personal loan for debt consolidation purposes, your lender may require a minimum credit score of 610 to 640. But some lenders may require an even higher score, like a 650, depending on the amount of money you're looking to borrow.

The higher your credit score, the more likely you are to get a competitive interest rate on a debt consolidation loan. If your credit score is lower than a 610, don’t give up. It’s still possible to qualify for a debt consolidation loan, so it's worth shopping around. However, you may end up with a higher interest rate.

Are there any Ohio state-specific debt relief programs or consumer protection laws?

In Ohio, a number of programs and laws are designed to protect consumers.

The Debt Adjusters Act of 2004 sets regulations for non-profits and other companies that offer credit repair services and debt counseling. The law makes it illegal for a credit repair or debt counseling service to accept more than $75 for an initial consultation or accept more than $100 a year for consultation fees.

The Credit Freeze Act of 2008 requires credit reporting agencies to allow consumers to freeze their credit to prevent new accounts from being opened in their names.

The Credit Services Organization Act of 2004 requires all credit repair or debt counseling services to be registered and bonded. It also gives consumers the right to cancel contracts with these organizations within three days.

Finally, the Homebuyer's Protection Act (Predatory Lending Law) of 2007 protects consumers from abusive lending practices. Lenders must make consumers aware of what payments they'll have for a mortgage, and they can only refinance an existing mortgage if the new loan comes with a reasonable benefit.

How to find reputable debt consolidation companies or credit counseling agencies in Ohio

To find a reputable debt consolidation company or credit agency in Ohio, start with the National Foundation for Credit Counseling (NFCC). The NFCC's website allows you to enter your information to connect with a certified counselor in your area.

The U.S. Department of Justice maintains a list of approved credit counseling agencies. You can use its website to find your judicial district by state and county, and from there get further information.

Check the credentials of any debt consolidation company or credit counseling agency you're thinking of using. Once you've narrowed down your choices, you can check them out with your state attorney general and the Better Business Bureau to find out if there are any complaints that have been filed against them.

Also make sure to ask plenty of questions when getting a consultation. And be wary of red flags, such as high upfront fees or high-pressure tactics to get you to sign a contract.

What are the pros and cons of debt consolidation for Ohio residents?

A big benefit of debt consolidation is having one fixed monthly payment instead of juggling multiple debt payments. Also, you may be able to lower the interest rate on your debt with a consolidation loan. If you're managing several credit card balances, for example, you may be able to lower your rate if you consolidate them into a personal loan.

A debt consolidation loan could also give you a clearer payoff timeline, which could help keep you motivated and on track. And if you make your consolidation loan payments on time, it could improve your credit score.

One downside of debt consolidation is that it won't wipe out any of your debt, and in some cases, it could cost you more in the long run. That's because the fees associated with a debt consolidation loan can add up. And if you're paying off your debt over a longer period of time, you might accrue more interest.

You might also struggle to qualify for a debt consolidation loan or one with a competitive interest rate, if your credit needs work.

How does debt consolidation affect my credit score in Ohio?

Debt consolidation could boost your credit score, but it could also bring it down. Making your debt consolidation loan payments on time every month could improve your credit score by helping you establish a positive payment history.

Also, in some cases, a debt consolidation loan might allow you to lower your credit utilization rate, which measures how much revolving credit you're using at once. That could benefit your credit score, too.

On the other hand, if you don't pay your debt consolidation loan on time, it could hurt your credit score. And if you consolidate your debt by using a credit card balance transfer, it won't help your credit utilization.

Also, any time you apply for a new loan, it triggers a hard inquiry on your credit report, which could cause your score to drop by a few points. However, if a debt consolidation loan makes it easier to keep up with your debt, timely payments could more than make up for the minor credit score hit a hard inquiry might cause.

What are the steps to apply for a debt consolidation loan in Ohio?

If you're looking for a debt consolidation loan in Ohio, start by checking your credit score and credit report. If you find mistakes on your credit report, try to get them corrected before you apply for a debt consolidation loan, since that could lead to a boost in your credit score.

Next, make a list of your various debts so you understand exactly what you owe along with their interest rates. Also gather financial information a lender might need, including pay stubs, bank statements, and proof of income.

After that, start shopping around for lenders in your area. Local banks and credit unions are a good place to start.

When comparing lenders, pay attention to the interest rate and loan terms each one offers, such as the length of your repayment period. Also make sure you understand the fees each lender will charge to put a debt consolidation loan in place and what your monthly payments will look like.

What alternatives to debt consolidation are available for managing debt in Ohio?

Debt consolidation has a number of alternatives you may want to consider.

With a debt management plan, you work with a credit counseling agency to roll your debts into one monthly payment. With debt settlement, your creditors agree to accept a lower amount than the total amount you owe.

You could negotiate a debt settlement on your own or with the help of a debt relief company. Debt settlement may be an option if you feel your debt truly isn't payable. However, debt settlement could have a negative impact on your credit score.

In some cases, budgeting carefully and using a debt payoff strategy could be an alternative to debt consolidation. If you're able to set a meaningful amount of money aside each month for debt payoff purposes, you can tackle your debts in order of highest interest rate to lowest, or smallest balance to largest—whichever method works best for you.

How do current economic conditions impact debt consolidation decisions in Ohio in late 2025?

Your credit score has an impact on the interest rate you might get on a loan, but so do larger economic conditions.

Right now, interest rates are still somewhat high. The Federal Reserve delivered its third straight interest rate cut at its final 2025 meeting. Rates dropped by a quarter point, which means we go into 2026 with the benchmark rate in the 3.50% to 3.75% range. Additional rate cuts could follow in 2026.

The lower the Federal Reserve's benchmark interest rate, the more affordable borrowing tends to be across the board. If you get a debt consolidation loan now, you may end up lowering the interest rate on your debt. If you wait until after the Federal Reserve cuts interest rates, you might end up with a rate that's even lower.

Also, the unemployment rate in Ohio has been trending upward. In March 2025, it was 4.8%, but as of August 2025, it was 5%. If you're not sure your job is stable, taking out a debt consolidation loan could be risky, since missing payments could damage your credit score.

End Your Debt

Find out how our program could help.

- One low monthly program deposit

- Settlements for less than owed

- Debt could be resolved in 24-48 months